Tax-Free Billions: Step by Step How Peter Thiel Has $5B in His Roth IRA

Few stories have captivated the public’s imagination quite like that of Peter Thiel’s Roth IRA. Here is the journey from a modest contribution of $1,700 to +$5 billion, step by step.

Swan Bitcoin IRA

Bitcoin is the ultimate asset for your retirement. Create a tax shelter for exponential returns! Get started in less than 2 minutes. Book a call with one of our Bitcoin IRA specialists today!

Schedule a CallThe Peter Thiel IRA Strategy: How $1,700 Became $5B

In 1999, before he became a billionaire, PayPal founder Peter Thiel had a Roth IRA worth $1,700.

Utilizing the proceeds from his substantial PayPal windfall and investment in Facebook startup shares, Thiel channeled millions into investments in other startups within Silicon Valley.

He even directed funds into his own hedge fund, as detailed in a memo from his financial assistant into his Roth IRA.

Here’s a breakdown of the Peter Thiel IRA strategy:

The process begins by opening a Roth IRA account. Even a relatively small amount is okay.

Swan IRA — Real Bitcoin, No Taxes*

Hold your IRA with the most trusted name in Bitcoin.

The next step is to seek out an opportunity to acquire an asset, or a stake in a startup company, that is expected to experience significant value growth in the future.

This step is crucial because the goal is to invest in a company whose shares are valued at a very low cost at the time of acquisition.

As with most startups, PayPal provided its key executives with modest initial salaries and substantial stock grants. Per Thiel’s IRS records, his earnings for that particular year amounted to $73,263.

Investors can use the money in their Roth IRA to buy low-value shares in a private company before it gets big ($0.00001). Some founders have used this strategy to buy shares in their own companies — with dirt-cheap prices set by the companies themselves.

Why do this?

Purchasing shares in a startup at a price per share that is extremely low, often just a fraction of a cent, allows them to acquire many shares with a relatively small investment for the greatest possible return on investment.

Sell your shares and keep all the profits tax-free in a Roth IRA account. The Peter Thiel IRA strategy acquired the ultimate edge any investor could have used but was a strategy that eluded almost all other investors:

Turning his personal investment bank into a Roth IRA, 100% shielded from taxation.

This newfound advantage allowed him to utilize the funds within his Roth IRA account to buy and sell nearly any investment he desired.

Investors can use the profits and gains to invest in new assets or securities within the Roth IRA.

Example: if you have stocks that have appreciated in value, you can sell them within the Roth IRA and use the proceeds to purchase new stocks or other eligible assets.

This strategy takes advantage of the Roth IRA’s unique tax treatment.

It opens up opportunities for individuals, including wealthy investors like hedge fund managers, industrialists, and heirs, to take advantage of the tax benefits offered by Roth IRAs.

As the startup grows in value over time, any profits generated from the appreciated stock within the Roth IRA remain shielded from taxes indefinitely.

** As long as a Roth IRA remains untouched until the investor reaches the age of 59 and a half (the age at which qualified withdrawals can be made without penalty), the earnings continue to grow tax-free.

Warren Buffet is universally recognized as one of the best investors ever. But, not even Buffet can’t hold a candle to the Peter Thiel IRA strategy.

Averaged a 20% annual return over 55 years.

Total Return: 5,828%

Averaged an annual return of 97% over 24 years.

Total Return: 294,117,600%

The Peter Thiel IRA strategy seized the opportunity to acquire shares in startups at remarkably economical prices. Thiel’s pivotal contribution of $500,000 marked the initial significant external cash infusion into Facebook.

Thiel’s Roth IRA is the largest account of its kind

Won’t have to pay a single penny in tax on this account

Can start to collect tax-free only six years from now

Interestingly, these very Facebook shares found their way—predictably—into Thiel’s Roth IRA, a fact later unveiled by a Facebook attorney through a letter submitted in a federal court.

This strategic move ensured the Peter Thiel IRA strategy wouldn’t be liable for taxes on his early investment in the social media giant.

At the time, Senator Roth assured that his novel IRA concept would, stating:

“Offer assistance to diligent, middle-class American workers.”

How would Senator Roth feel about Peter Thiel’s IRA portfolio today?

Transforming the Traditional IRA: The Roth Conversion

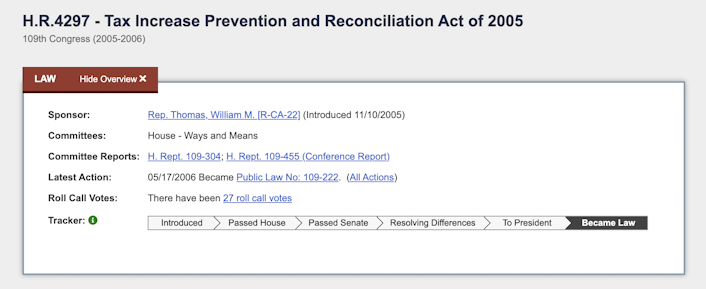

About a decade after the creation of the Roth, changes introduced a backdoor method for investors to convert a traditional retirement account into a Roth IRA by paying a one-time tax.

This conversion option was introduced through the Tax Increase Prevention and Reconciliation Act of 2005 (TIPRA) and became effective in 2010.

The newfound flexibility significantly impacted retirement planning by allowing individuals to shift their retirement savings from a tax-deferred environment to a tax-free one.

It allowed any American to take money in less favorable traditional retirement accounts and, after paying a one-time tax, to shift them to a Roth where their money could grow untaxed, similar to having your own Bermuda-style tax haven right here in the U.S.

This process was a significant departure from previous restrictions that limited Roth conversions to individuals with lower income levels.

Before the change:

Individuals were limited in converting their traditional IRAs to Roth IRAs.

It expanded retirement planning options and gave individuals more flexibility in managing their retirement savings.

It also changed the tax code and allowed individuals to convert their traditional IRAs into Roth IRAs.

Removed the income limitation previously preventing high-income earners from converting their traditional IRAs into Roth IRAs.

Before this change, only individuals with a modified adjusted gross income (MAGI) of $100,000 or less were eligible to convert. Now, regardless of income, anyone could convert their traditional IRAs into a Roth.

NOTE: When an individual converts a traditional IRA to a Roth IRA, they are required to pay income tax on the converted amount in the year of conversion. This is because the funds in the traditional IRA were contributed pre-tax, and the government wants to collect the tax revenue it would have received upon withdrawal.

The decision to convert to a Roth IRA depends on several factors:

Future tax rates

The individual’s financial situation

Retirement goals

So, what does this mean for you?

In his book “Zero to One,” Thiel argues that fortunes are built not by luck or unfair advantage but by discerning investors and founders who are more courageous than their peers, leaders who zig when the crowd zags.

Thiel devotes an entire chapter to the importance of keeping secrets, writing that “every great business is built around a secret that’s hidden from the outside.”

By 2019, Thiel’s holdings were so vast and diverse that his +$5 billion was spread across 96 sub-accounts inside his Roth. These retirement account strategies all relied on publicly traded investments and strategy available to all taxpayers…

You won’t make $5B dollars like Thiel, but could you make $5M? Absolutely!

Compound Interest: Humanity’s Greatest Shortcoming

Investing for retirement is a journey that requires careful planning, patience, and a good understanding of the dynamics of compound interest.

“The greatest shortcoming of the human race is our inability to understand the exponential function.”

- Albert Allen Bartlett

One question often arises in investors' minds: How often does money typically double in an IRA?

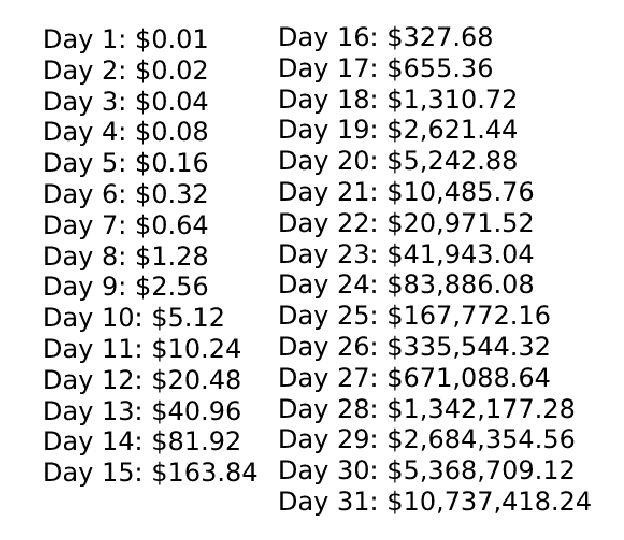

Simple Example: Would you rather have $5M all at once or a penny that doubles daily for a month?

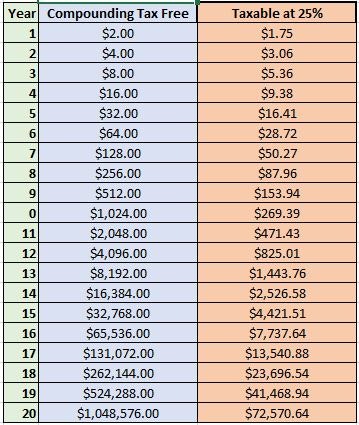

Unlike simple interest, which is calculated solely on the principal amount, compound interest also takes into account the accumulated interest.

As your interest earns interest, your account experiences exponential growth

This phenomenon can lead to significant financial gains over the long term

When shaping a robust retirement portfolio, including Bitcoin might initially raise eyebrows. Often linked to its fair share of volatility and perceived risk, Bitcoin presents an array of reasons why it should be considered a prudent long-term investment for your IRA.

Diversifying your IRA with assets that promise substantial returns, like Bitcoin, can be a shrewd move. The inherent advantage lies in the potential for tax-deferred or even tax-free growth, depending on your IRA type — whether traditional or Roth.

While you likely won’t be able to turn your Roth IRA account into a $5B; a $5M Bitcoin Roth IRA account, perhaps. Bitcoin can provide you financial security using the Peter Thiel IRA strategy.

To see what may happen to your returns after adding Bitcoin to your retirement portfolio… Run your own numbers with our open-source Bitcoin Retirement Calculator.

This is part of a new initiative called Swan Research.

The conventional retirement portfolio often follows a 60/40 allocation between stocks and bonds, a strategy designed to balance risk and reward. Bitcoin, however, takes diversification to the next level.

Unlike traditional assets, Bitcoin exhibits a lower correlation, making it a valuable addition to your portfolio.

This can ultimately enhance your overall risk-adjusted returns, offering an edge in unpredictable market conditions.

The insidious effects of inflation on the purchasing power of your hard-earned money over time are undeniable.

Bitcoin is a potential safeguard against the erosion of value caused by unrestrained monetary expansion from newly issued banking credit and government deficit spending into the total supply.

With a fixed maximum supply of 21 million coins, Bitcoin’s scarcity sets it apart from fiat currencies susceptible to devaluation and even physical gold.

In June 2022, authorities in Uganda revealed a significant find of around 31 million metric tonnes of gold ore within the nation. This discovery could yield up to 320,158 metric tonnes of purified gold, with an approximate valuation of $12 trillion.

This single new discovery represents more than the entire amount of gold above ground and accounted for in total supply. As this gold is recovered, it will begin to significantly dilute the scarcity properties of the metal.

However, no one will ever find a single additional satoshi of new Bitcoin. New massive gold deposits like that recently discovered in Uganda will continue, though.

Predictive models indicate that the final Bitcoin will be mined by 2140, over a century away.

In contrast, NASA, the U.S. government’s space research agency, has devised a strategy to capture an asteroid valued at $10 quintillion, primarily due to its abundant precious metals like gold.

NASA’s timeline suggests that the asteroid retrieval mission could occur in late 2029 or early 2030, assuming the mission is successful.

Contrast the conventional 7% expected annual returns of a standard 60/40 portfolio with the impressive track record of Bitcoin.

Above, we mentioned that the Peter Thiel IRA strategy has netted an average return of 97%. Since its inception in 2009, Bitcoin’s average annual price increase has exceeded 100%, showcasing its potential for monumental growth.

While it’s prudent not to put all your eggs in one basket, even a small allocation into a Bitcoin IRA can significantly bolster your retirement prospects.

A Rollover is a movement from a 401k, 403b, or similar retirement account to a Roth IRA usually coordinated primarily by the customer and their existing retirement custodian.

Typically funds are sent by wire transfer, which is the recommended method. Funds can also be sent via cheque. However, this is significantly slower than sending funds via wire transfer.

Before completing a rollover, you must liquidate your other retirement account to cash. You can initiate a Rollover via your current custodian.

Can I roll over part of my 401k, 403b, or similar retirement account into Swan IRA?

To see your Swan IRA Rollover instructions, click on "Rollovers" on the Navigator bar of your Swan IRA account.

While the IRS allows partial rollovers, some employer-sponsored plans may not permit them.

Contact your plan administrator to confirm whether your plan allows partial rollovers.

What is the pricing of the Swan IRA?

A 0.99% transaction fee taken out when the funds are moved over.

Interested in speaking to an IRA expert?

A Swan Bitcoin IRA compares very well against other Bitcoin investment sites.

If you are interested in a tax-free Coinbase alternative or have any other questions, please email IRA@swanbitcoin.com.

Book a call with a rep today and get a personalized guide on how to maximize your retirement portfolio with Bitcoin.

If you liked this content, check out the Swan Signal blog.

Swan IRA — Real Bitcoin, No Taxes*

Hold your IRA with the most trusted name in Bitcoin.

More from Swan Signal Blog

Thoughts on Bitcoin from the Swan team and friends.

MSTR vs. GBTC Compared: Which is Best in 2024?

This article compares MSTR and GBTC, offering insights for investors by examining their features, benefits, performance, fees, and drawbacks, focusing on their role in Bitcoin investment strategies.

Changing Bitcoin: The Past, The Present, and The Future (Part One)

For Bitcoin to achieve the lofty goals many have for it, its rules will need to change. This three-part series of articles will tackle what it takes to change Bitcoin.

4 Reasons to Avoid Coinbase In 2024?

The crypto platform is facing all kinds of problems. Is it time for customers to seek out an alternative?